By Andy Meeks, February 25, 2021

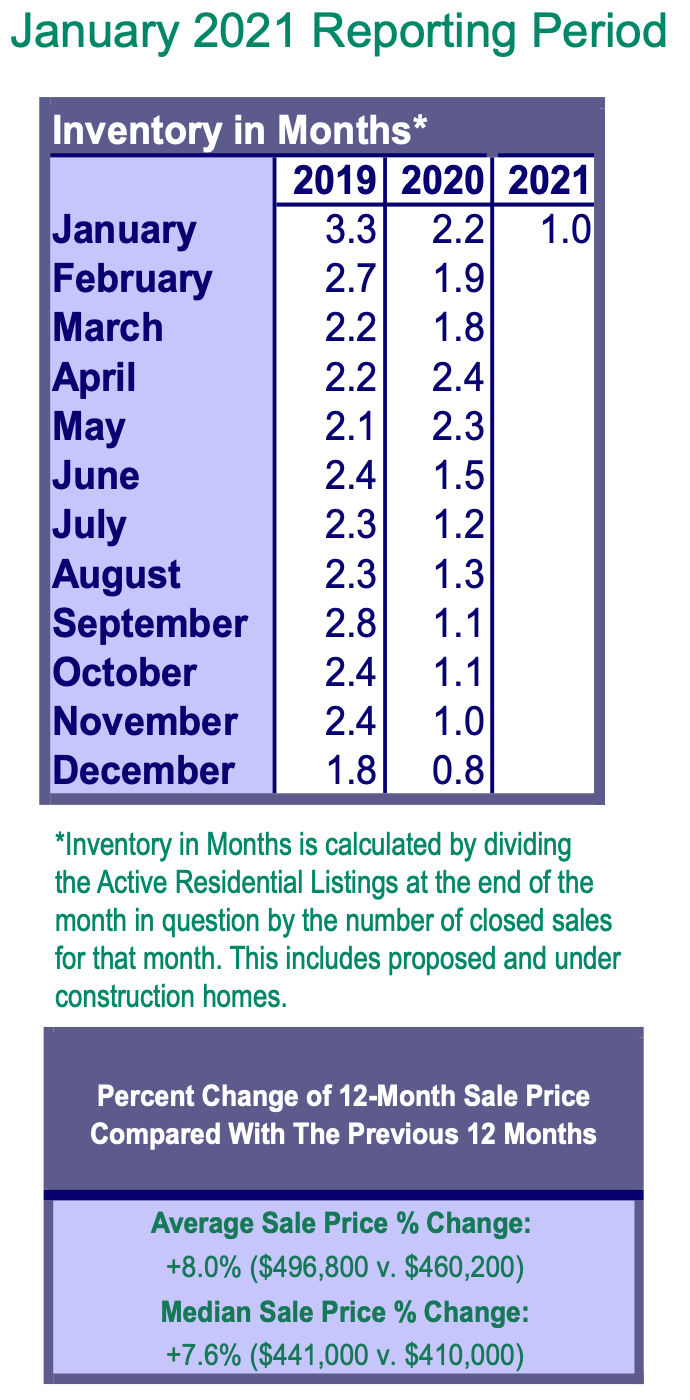

By every metric, we are in the midst of one the most active and competitive markets in Portland real estate history. We are facing a perfect storm of massive buyer demand, buyers with very strong buying power, and historically low inventory. This has resulted in average year-over-year sales appreciation rates at more than double what is considered ‘normal’. Homes at nearly every price point are selling with multiple offer situations, and almost nearly always at prices above asking price…anywhere from 7-10% for your ‘average’ home to more than 20% for your special ‘unicorn’ homes that are highly desirable. And that goes for homes at nearly every price point in almost every part of town.

The Law of Demand & The COVID Effect

The law of demand states that the higher the price of a good, the less of a demand there will be from buyers. However, this is not what we’re seeing. It’s because there is a more inelastic demand when it comes to homes…if you need to move, you need to move, and you will end up paying to do so. So beyond the record low mortgage rates giving buyers unprecedented access to borrowing money cheaply (and thus increasing their buying power), the COVID pandemic has pushed many more people into the market than normal as their living situations have changed quickly, unexpectedly and seriously. Buyers need more space for homes offices, for classrooms for their children, room for family members to stay long-term, better outdoor spaces for gathering and entertaining safely, or more space from their neighbors. These needs are hard to put off for long, and so the influx of buyers has been greater than the new inventory coming on the market for sale. People are also perhaps less likely to sell when they’re not sure where they’d go during a pandemic or how they’d pay for their replacement property when prices are so high, or they’re postponing the retirement or the empty-nester downsizing, or simply don’t want people coming through their home while they’re living there. Any way you cut it, there are many more buyers than there are sellers.

Build A Strategy Based Upon Your Assets As A Buyer

And that’s made it very difficult to be a successful buyer in this market, unless you’re able to make an all-cash offer with no contingencies. (And there are lots of those buyers out there, as well!) So how does your average buyer — someone who has saved for a 5, 10, or 20% downpayment and needs to finance the remainder of the purchase through a conventional mortgage — compete in this market and successfully purchase a home? You need to be able to grind away at seeing lots of homes, get comfortable with being a bit uncomfortable when making offers, and have a solid strategy in place. That strategy should take into account your assets as buyer; i.e. the tools you have at your disposal, whether it be tangible assets or your risk tolerance (and hopefully some combination of both). The question is always: how can you set yourself apart from other buyers?

How To Flex The Offer In Your Favor

Below is an explanation of various terms in an offer than you might be able to flex in your favor. Every strategy presented by these will be on the risk/reward spectrum, and not all of these are available or desirable for everyone. But it’s important as a buyer to understand how these terms can be used to your advantage and should be considered and discussed with your broker and lender as you get involved in the market as a homebuyer.

- Offer price: this is the obvious one, but figuring out how much to offer while not offering too much is never easy. Of course, it will always come down to your desire, willingness and ability. Figuring out what the right number will be requires a combination of analyzing comparable, recent sales, but also understanding how far you need to stretch to make a seller say Yes. Real estate brokers who are submitting offers for their clients frequently will have a good grasp of what that winning number will be. Also important to remember: the highest offer price is no guarantee of success. There are many other factors when considering the strength of an offer, and very often a combination of other great terms can overcome not offering the most money.

- Type of financing: if you’re a cash buyer, you can stop reading now and congratulations to you…you’re going to have a huge advantage over every other buyer out there. If you’re not a cash buyer, how much are you financing? Larger downpayments, of at least 20%, can have the advantage of perhaps qualifying the property for a waiver appraisal (if the property was sold or refinanced in the last 7 years). More on the appraisal below, but in addition, larger downpayments can also instill greater confidence in sellers as it relates to the quality of the buyer as a borrower, which makes them perhaps more likely to make it through the underwriting process successfully.

- Choice of lender: in a smaller market like Portland, reputation is paramount, and local lenders will always be able to provide a boost to your offer. Large national banks and lenders may advertise great rates, but they have some well-earned and poor reputations for not being able to close loans on-time, and for marginal customer service. If you can’t close on-time as a buyer, you’re in breach of contract and you risk losing your earnest money deposit. A lender who know the Portland market, who is accessible and communicates well, and who will always be available to help, is a crucial asset and team member in your homebuying campaign. Choose wisely.

- Closing date: if you’re financing your purchase, the typical closing timeline is usually 28-30 days. But if you and the property can qualify for an appraisal waiver, then you might be able to shorten the closing date by 7-10 days or more. And that’s a big advantage. Cash buyers win here again because they don’t need more than a few days at most to close, pending any inspection period, etc. Speak with your lender to understand what their ability is to close fast.

- Order appraisal quickly: the appraisal is often the one step in the process that takes the most time, so in order to guarantee you can meet your selected closing date, it’s crucial to order the appraisal as soon as possible…ideally upon mutual acceptance of the sales contract. The risk to this is that as soon as the appraisal occurs, the buyer is on the hook to pay for that appraisal. And they can cost anywhere from $750-1000. This cost is wrapped into the buyer’s closing costs, so if often invisible in that way, but if for some reason the deal doesn’t close, the lender may pass along that cost to the buyer to pay out-of-pocket (although many lenders can waive this or wrap it into the next transaction). Definitely ask your lender how it works for them.

- Address specific seller needs: it’s important to know whether the sellers need anything in addition to ‘best terms’ [offer price, closing date, inspection/appraisal waivers, etc.]. One of the most common things is the need for ‘rent-back’ while they find a new home and move out. If you have flexibility in your current living situation, and can offer free or cheap ‘rent-back’, basically making the sellers your new tenants at closing for a period of time (but usually no more than 60 days), that can help strengthen your offer considerably.

- Inspection waiver // set minimum repair figure: perhaps you’re very handy, have a family member or friend who is a contractor or in the trades, or you have a good feeling about a home after viewing it, or simply are less risk-averse. If so, you may offer to waive the home inspection and environmental inspections, or some combination, and promise to purchase the home as-is and not request any repairs. Risky, for sure, but this can be a big difference maker. Or, short of a full waiver, perhaps you offer to not request any repairs less than a certain dollar amount. Either way, these terms can trim some risk from the seller, and that has considerable value.

- Appraisal gap coverage // appraisal waiver: this is where it start to get tricky, and often a bit uncomfortable. But this is probably the single biggest term to get right. If the purchase is being financed, it needs to have an appraisal. The appraisal is an opinion on the value of the home, and the lender hires the appraiser to help support the loan under consideration. If there is a shortfall between the sales prices and the appraised value — and this is happening frequently in this market because of the high sales prices — it’s a risk to the transaction because of the appraisal contingency in the contract that provides protection for the buyer and an ability to terminate if the property doesn’t appraise at the sales price. This potential gap in value makes sellers nervous, and you definitely need to address this in your offer, if at all possible. How this works is more complicated and beyond the scope of this blog post. But, very basically, a buyer can provide assurances that they will close any gap between the sales prices and the appraised value. This is done by increasing the downpayment by that difference to preserve the loan to value ratio that’s desired or required. So, if you have extra cash beyond what you set aside for your downpayment, and are able to deploy it in this manner, it can be hugely beneficial to you.

- Release earnest money early: the earnest money deposit is the consideration a buyer provides to the seller to choose their offer and negotiate exclusively with them through the process. This earnest money is typically 1-2% of the purchase price, and acts as liquidated damages in case the buyer backs out of the transaction outside the various contingencies in the contract. It’s what the seller keeps if the buyer can’t close the loan on time or gets cold feet. The earnest money deposit is part of the downpayment, so you’re simply paying it forward to your downpayment that’s needed at closing. You can potentially structure your offer so your earnest money is unconditionally released to the sellers at various milestones during the transaction. Of course, there are significant risks with this, but if you’re 100% committed to buying the house, this might be a method that can benefit you.

Good luck out there, and let me know if you have any questions!

Andy Meeks

Principal Broker | OR

My clients are always my top priority, and my singular focus is their success. This is the intention I set every day.

My training and background as a licensed attorney helps me lead with a sharp attention to detail, a keen ear and focused voice, and an unwavering commitment to integrity, transparency and discretion.

I’m a passionate advocate and I thrive when helping others succeed, and I’m always available to connect over a cup of coffee to learn how I can help make good things happen.

Read my client reviews here.

The choice to become a real estate broker was a joyful combination of two very different careers. Prior to moving to Portland in 2008, I was an environmental and title closing attorney in Massachustts. Since then, I've served as a program manager and fundraising professional for Portland-based non-profit organizations Friends of Trees, The Freshwater Trust and Ecotrust.

While not scouting homes and helping clients, you can find me riding bicycles, skiing, digging in the garden, experimenting in the kitchen, and exploring the stunning beauty of the Pacific Northwest.

Please let me know how I can help you or someone you know. Thank you!

*I'm licensed as an attorney in Massachusetts and can't offer any sort of legal advice.

Read More